The bulk of the market’s growth no longer depends on a stagnant exit market, but on a structural change in the way private equity firms manage their portfolios

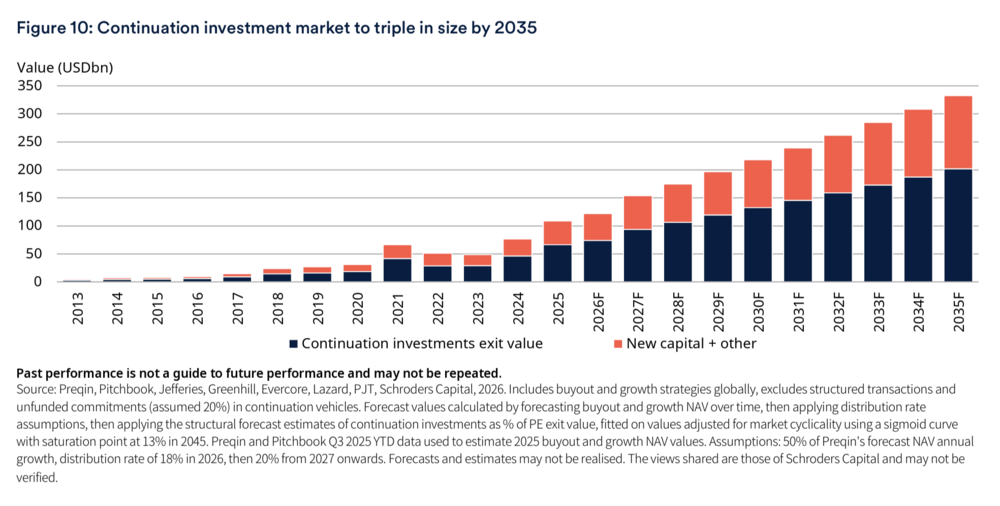

Schroders Capital Report “Continuation investments continue to grow – and to reshape the buyout market” by Nils Rode (Chief Investment Officer), Petr Poldauf (Senior Investment Director) and Eufemiano Fuentes Perez (Lead Data Scientist) says that in 2025, continuation funds deals hit an above analysts’ expectations peak of 109 billion US Dollars (76 billion US Dollars in 2024). In the baseline scenario, the authors predict that by 2035 the market could exceed 330 billion US Dollars per year, more than triple than the current amount (press release).

Schroders Capital highlights that the most interesting data to emerge is not so much the growth itself, but rather its nature. The cyclical component of this expansion linked to the difficulty of selling portfolio assets through traditional channels (IPOs and trade sales) fell from 14% in 2024 to 9% in 2025. Therefore, th bulk of the growth no longer appears to depend on a stalled exit market, but rather on a structural change in the way private equity firms manage their portfolios.

The assets owners change instead of the ownership length

Schroders Capital begins by analysing a structural constraint: a private equity fund has a limited contractual lifespan, and if, upon expiry, a company is not yet ready for a trade sale or an IPO, the only way to keep it within the ecosystem has always been to sell it to another asset manager through a secondary buyout. The sponsor-to-sponsor transaction accounted for an average of 38% of deals and 36% of their total value, according to Schroders Capital’s analysis of two decades’ worth of data.

In a secondary buyout, the original fund usually carries on a full exit. The general partner (GP) changes as well as the strategy could. Continuation investments, on the other hand, address the same constraint (a fund reaching the end of its life, a company not yet ready for a definitive exit) with a different solution: the same manager creates a new vehicle to acquire the asset, retaining control and injecting fresh capital through the lead underwriters. Schroders Capital describes continuation investments as a “partial substitute” for secondary buyouts as they address the same underlying demand: a more cost-effective and efficient alternative solution for the same problem. The report’s estimates that this type of entities will account for around 5% of the total deal flow in medium- and large-sized buyouts over the next ten years, with a significant impact on large buyout managers and secondary firms.

A third of the portfolio companies is ‘ready’ for continuation

Schroders Capital analysed around 2,600 completed buyout transactions and calculated the total value to paid-in capital (TVPI) for each of them on a logarithmic scale. More than 31% of the buyout funds’ portfolio companies is statistically fit for a continuation investment as it generated an above 2X multiple – the typical least return threshold that both secondary buyouts and continuation deals require – without necessarily needing a change of control for continuing its transformation.

Why it’s beneficial for investors: less risk, greater liquidity, lower fees

The report highlights the benefits for investors in these vehicles compared with traditional buyouts:

- faster liquidity: continuation investments have a shorter holding period of around 1.5 years compared to traditional buyouts (less than three years versus over four), equating to a liquidity period that is around 35% quicker;

- lower management fees: continuation vehicles charges are worth about half of those of traditional buyout firms (1% per year on the net invested capital vs 1.9% median on secondary buyouts committed capital – Preqin) and their carried interest has a tiered structure. On the ground of 2025 volumes, Schroders Capital estimates that the total savings for investors resulting solely from lower fees amount to approximately 5.7 billion US dollars;

- more predictable returns: a research of Evercore on 387 continuation funds established between 2018 and 2024 shows returns comparable to those of traditional buyouts, but with significantly lower variation in results.

The lower mid-market is the most fertile ground

Schroders Capital says that the most attractive segment for continuation investments is the lower mid-market – companies with an enterprise value of less than one billion US Dollars, and in particular those below 750 million – where more than two-thirds of the potential continuation transactions that the firm assessed in recent years operate. There are two reasons for this: on the one hand, deal sourcing in this segment is far less reliant on secondary buyouts (less than 25% of investments come from other funds, compared with a much higher proportion in the larger size brackets); on the other hand, smaller companies offer greater potential for transformation and greater resilience during periods of market stress.

Estimates for 2035: between 290 and 505 billion US Dollars

Schroders Capital base scenario grounds on a conservative growth of private equity’s NAV (in the region of 6.5% per year, half of Preqin estimates) and on a distribution rate which is stable at around 20% of NAV. In these conditions, the continuation funds market could be worth above 330 billion US Dollars in 2035 and such investments could weigh about 12% of all private equity distributions vs a historically stable proportion of 36% for secondary buyouts. In a low case scenario, the market size could be worth 290 billion US Dollars, almost three times as much as in 2025. In a more optimistic context (high case) such a figure could be of up to 505 billion US Dollars, almost five times current levels. However, buy-side player should have enough capital to fund such a growth.

{kind=link}

{kind=link}