DC Advisory highlights that market operators closed 79 transactions in Italy out of a total of 1052: acquisition finance (42.9%), refinancing and recap

In 2024, the European leveraged finance market recovered strongly with record levels of transactions worth 207 billion that overtaken the 2017 peak of 158 billion, PitchBook European Credit Markets Quarterly Wrap said. Refinancing and repricing activities (57% of total volume) boosted the figures. A wave of CLO (Collateralized Loan Obligations) issuances worth 45 billion that compressed spreads and made credit more accessible fuelled such favourable conditions.

DC Advisory‘s European Debt Market Monitor argues that such a positive trend may continue in 2025 in light of lower interest rates and m&a activity uptick.

DC Advisory mapped 1052 leveraged finance transactions for 2024, 42.9% of them supported LBOs while the other have been refinancing or recapitalisation deals. The mid-market segment volumes amounted to 319 deals in 2024 (257 in 2023), while the aggregate value of acquisition finance reached 40.3 billion and doubled from 2023, but still below the 10-year average. In addition, the private credit market faced the competition of syndicated loans that crunched the margins.

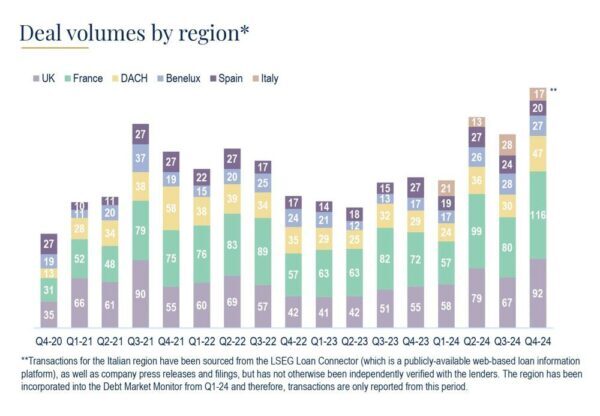

DC Advisory said that in 4Q24 17 Italian companies attracted pool financing facilities, downs from 28 firms in 3Q24, for a total of 79 deals with banks and private debt funds in the whole year. Market participants closed in Italy refinancing deals (52.9%) and LBO (47.1%). The majority of these have been unitranche deals (64.7%) and banking pools (23.5%). Intesa Sanpaolo (30 deals), Unicredit (28), Banco BPM (24), and BPER (22) have been the main players. CA-CIB, BNP Paribas, Tikehau (6), Pemberton (6), Eurazeo (5), Blackstone (4), and Muzinich (4) closed a relevant number of deals.

The French market closed 2024 with an all-time peak of116 transactions in the fourth quarter bringing the total to 352 transactions for the year. This occurred despite the political instability after the Barnier Government crisis. The boost came from refinancing (53.4% of transactions). Banks Société Générale (112 deals), BNP Paribas (107) and LCL (93) and funds CIC Private Debt, CAPZA and Eurazeo have been the most active players.

The UK and Ireland recorded a 37% increase in volumes in 4Q(92 deals compared to 62 in Q3), bringing the year-to-date total to 296. A better rate environment and a decrease in political uncertainty following Labour’s victory driven such a boost. Ireland also maintained solid activity grace to stable m&a and refinancings. HSBC (50 deals), Barclays (30), Lloyds (15), Ares, Apollo, and Pemberton have been the most active players.

In 4Q24, DACH region (Germany, Austria, Switzerland) deals also sharply increased from 30 to 47 (+50%), bringing the total for the year to 137. Refinancing operations made the majority of transactions (61.7%), but market players expect LBOs to pick up in 1H25. NordLB, OLB, LBBW, ING, Ares, Eurazeo, and Arcmont have been the most important players.

Spain experienced an exceptional 2024, exceeding the financing volumes of 2021 and 2022 and reaching a total of 90 transactions. The distribution of LBOs and refinancings has been almost even (45% and 55%). The main banks active in the market were CaixaBank (34), Santander (32) and BBVA (30). Domestic funds such as Tresmares and Oquendo, along with international competitors such as Ares also played a relevant role.

The Benelux market remained weak in 2024, down 3% from 3Q24 (27 deals from 28), settling at 98 deals for the year. A recovery could only take place in 2H25. Much of the activity involved refinancing transactions for fetching cash. OLB, ING, Rabobank, Permira, Ares, and Tikehau supported the activity.

For 2025, DC Advisory expects refinancing and repricing activities to continue, grace to falling rates and a pick-up in m&a that the funds will support for deploying their capital and their 1.3 trillion worth dry powder.

{kind=link}