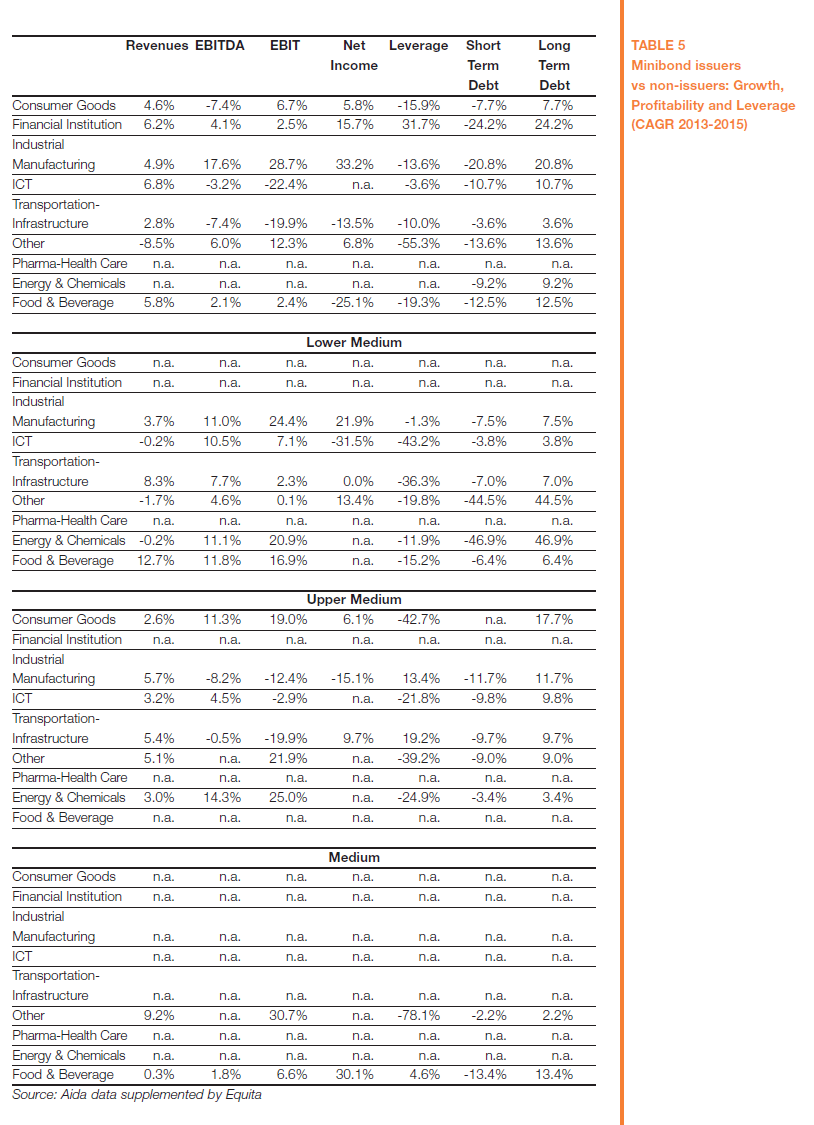

Investing in Italy does pay both on equity and on debt side. And as for debt, SMEs issuing so-called minibonds grow at a higher pace than their competitors both in revenues and ebitda.

Investing in Italy does pay both on equity and on debt side. And as for debt, SMEs issuing so-called minibonds grow at a higher pace than their competitors both in revenues and ebitda.

This is the evidence of a study by Equita sim and the Baffi Carefin department of the Bocconi University in Milan, which was presented yesterday by Stefano Caselli, Bocconi Vice Rector, and Stefano Gatti, director Full Time Mba, Sda Bocconi, together with Equita simìs top management.

The study compares compound annual growth rates of revenues, profitability, leverage and debt tenor over the period 2013-2015 of minibonds issuers with respect to the changes in these same variables across a sample of size- and industry- matched non-issuing firms. Issuers experience a superior growth in revenues than non-issuers. For all but small size issuers abnormal growth in revenues is accompanied with a superior growth also in ebitda.

As for the Italian listed equity, in the period between 2006 and 2016 investors would have obtained quite good yields if they had focused the most on medium size companies active in made in Italy sectors such as fashion, food&beverage or automotive. Actually the Ftse Star Index recorded am average 2% annualized performance for a buy-and-hold strategy in the period plus an average 2.7% each year due to dividend policy.

This good performance was seen also on the private equity side, with an average gross Irr for Italian private equity funds of 8.8% in the period (see Aifi-Kpmg data).

As for the listed corporate debt, the Italian paper guaranteed higher yields that other euro countries’ paper, due to the sovereign crisis and a higher country riscj associated to Italy even if companies’ fundamentals are quite strong as a very low default rate shows.

{kind=link}