CDP Equity (CDPE), KKR (through Teemco Bidco srl), Macquarie Asset Management, Open Fiber and TIM have signed a non-binding Memorandum of Understanding (MoU) aimed at creating a single, non-vertically integrated telecommunications network operator merging TIM and Open Fiber’s networks (see here the press release). The parties have undertaken to negotiate exclusively and in good faith the terms and conditions of the transaction with the aim of reaching the signing of the binding agreements by next 31 October.

CDP Equity (CDPE), KKR (through Teemco Bidco srl), Macquarie Asset Management, Open Fiber and TIM have signed a non-binding Memorandum of Understanding (MoU) aimed at creating a single, non-vertically integrated telecommunications network operator merging TIM and Open Fiber’s networks (see here the press release). The parties have undertaken to negotiate exclusively and in good faith the terms and conditions of the transaction with the aim of reaching the signing of the binding agreements by next 31 October.

The announcement, which arrived late yesterday evening, follows the one of early April, when TIM had signed a confidentiality agreement with CDP Equity (see here a previous article by BeBeez) to start the preliminary discussions regarding the possible integration of the TIM network with the Open Fiber network, of which CDP Equity holds a 60% stake with the rest in the hands of Macquarie infrastructure since last December 2021 (see here a previous article by BeBeez). At that time, the date of April 30 was pruned as an indicative deadline for the signing of the memorandum of understanding.

The objective of the MoU is to launch a process aimed at creating a single operator of the tlc networks, not vertically integrated, controlled by CDPE and participated by Macquarie and KKR, which allows to accelerate the spread of optical fiber and VHCN infrastructures (Very High Capacity Networks) throughout the country, thus allowing access to the most innovative and efficient services offered by the market to the general population, public bodies and businesses.

More specifically, the transaction envisages that in the first instance TIM’s infrastructural activities of the fixed network will be separated from the commercial ones and that as a second step these infrastructural activities of TIM will be integrated with the network controlled by Open Fiber. As a result of the transaction, TIM will be able to focus its activities on telecommunications and data transmission services on the Italian market as a priority.

Recall that Open Fiber manages the largest Italian FTTH network, serving more than 12 million families in over 180 urban centers and more than 2,300 rural areas across the country. It also guides the spread of ultra-fast broadband throughout Italy. Based in Milan, last December it launched the new industrial plan 2022-2031, which foresees around 11 billion euros of investments for the coverage with the latest generation network of around 24 million real estate units (IU) of over 13 million IU current and to support the growth of the customer base, in line with the plan target which provides for the achievement of the take-up target of 50%. These investments will be covered by the extension of the financing to 7.175 billion euros, by equity and cash generation. At the end of the plan, a margin of over 75% is expected, with revenues of over 2 billion euros. Break even (ebitda net of investments) is expected in 2026.

All this without, however, counting the effects of an integration with the TIM network. We recall, in fact, that for some time the Open Fiber story has been intertwined with that of FiberCop, the new company into which TIM’s secondary network (the so-called last mile, from the cabin on the street to the homes) and the fiber network developed by FlashFiber, TIM’s joint-venture (80%) with Fastweb (20%), and in which the KKR Infrastructure fund acquired 37.5% in April 2021, investing 1.8 billion euros, based on an enterprise value of approximately 7.7 billion euros, while Fastweb obtained 4.5% in exchange for the contribution of its stake in FlashFiber (see here a previous article by BeBeez). The entry of KKR and Fastweb in the capital of FiberCop has always been considered the first step towards the realization of a broader project for the establishment of a single company in the national network, necessary for the development of digital in Italy, which should have involved OpenFiber .

Regarding the involvement of KKR in the operation, we remind you that, once the hypothesis of a takeover bid by KKR on the entire capital of TIM faded, again at the beginning of April (see here a previous article by BeBeez), KKR had left the door open to other options, declaring that “in any case it is willing to explore any other operation in the interest of the Company, its shareholders and the country”, which was read as the desire to be involved precisely in the operation of creating a single tlc network .

Moreover, the boards of directors of TIM and Cassa Depositi e Prestiti already in August 2020 approved a letter of intent between TIM and CDP Equity aimed at integrating FiberCop with OpenFiber to give life to AccessCo, a company also open to other investors and destined to manage the single national network. AccessCo was to be established through the merger between FiberCop and Open Fiber (see here a previous article by BeBeez). But then that letter of intent remained in the drawer.

That the project was accelerating, however, had been clear for a few days. In particular, some weeks ago, on the occasion of his speech at the Bloomberg Italy Forum, Francesco Giavazzi, an economic advisor to the Prime Minister, said: “The single network is one of the objectives of the government and it will happen”. The confirmation of a squeeze on the project also came from Cassa Depositi e Prestiti. In fact, the managing director Dario Scannapieco said: “Duplication of investments on the network makes no sense from an industrial point of view. We carefully monitor the evolution of a strategic sector for Italy” (see here a previous article by BeBeez).

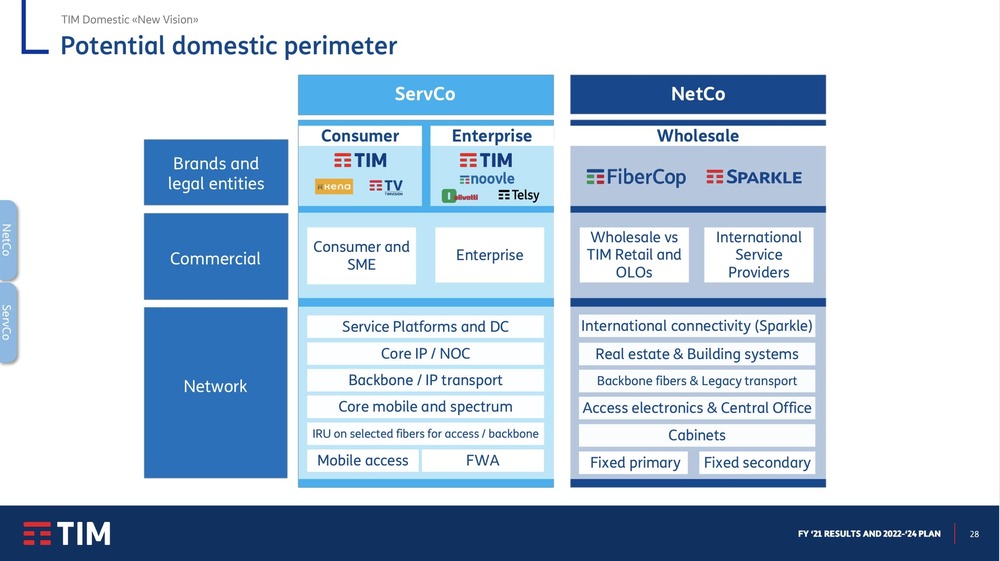

The structure of the first part of the transaction, i.e. the separation of TIM’s fixed network infrastructural activities from the commercial ones has not yet been defined, but we remind you that at the end of March CVC Capital Partners had delivered a non-binding offer to the tlc group’s Board of Directors for 49% of the Enterprise area of ServCo, the newco of services of the TIM group, which will be born after the separation from Netco (network and Sparkle), according to the spin-off project envisaged by the ceo Pietro Labriola (see here a previous article by BeBeez). The offer, according to reports from several sources, would value the Enterprise area at about 6 billion euros, including debt, that is a figure that is a little above the minimum of the broad valuation range of 5-10 billions calculated by some analysts. We recall that the 2021 aggregate turnover of the activities that will form the Enterprise area of ServCo was approximately 2.7 billion euros out of the total of 9.9 billion of the entire ServCo (see the presentation to the analysts here) with an ebitda margin 27/28%, or 730-760 million euros. On this basis, Bestinver calculated, with a multiple EV/ ebitda 2022 of competitors equal to 15x and considering that in the ServiceCo the ebitda 2022 should deteriorate slightly, that “we would end up with an EV of about 10-10.5 billion euros for the business enterprise”. Moreover, in the meantime, rumors relating to an interest in the same dossier by Apax Partners returned to circulation, as reported on these pages at the end of March (see here a previous article by BeBeez).

{kind=link}