Trevi Holding S.E., the majority shareholder of the Trevi Finanziaria Industriale (Trevifin) civil engineering group, submitted a so-called blank settlement request (concordato in bianco or concordato con riserva) to the Court of Forlì-Cesena, with the aim of reaching a debt restructuring agreement pursuant to Article 182-bis of the Italian Bankruptcy Law (see Il Resto del Carlino here).

Trevifin, specialized in underground engineering and in the drilling sector, is listed at the Italian Stock Exchange and is held as for a 16.60% stake by FSI Investimenti spa (controlled by Cdp Equity, an investment veichle controlled by Italy’s National Promotional Institution Cassa Depositi e Prestiti) as for a 10% stake by US investment fund Polaris Capital Management, and as for a controlling 32.73% stake by the Trevisani family (through its Trevi Holding SE). The initiative, said the company in its press release, is aimed at guaranteeing Trevi Holding “the right framework in which to seize the investment opportunities that may derive from a favorable outcome of the due diligence in progress by the investment funds interested in supporting financially the company in the Trevifin recapitalization deal “. The recapitalization was announced last December and relates to a capital increase of 440 million euros, of which 130 millions in cash by current shareholders and 310 millions thanks to the conversion of part of banking loans into equity (see here a previous post by BeBeez).

In detail, then the FSI and Polaris shareholders had confirmed that, under certain conditions, they would subscribe he share of the capital increase due to them by virtue of their respective option rights and that they would ensure the subscription of a further stake of any unopted share to to the maximum amount of 38.7 million euros each, that is to say a total of 77.4 million out of the total 130 million euros cash. The subscription of the remaining share of capital increase amounting to 52.6 million euros would be guaranteed, in the event of unopted shares, by a guarantee consortium organized by the lending banks, through the conversion of loans as part of the above conversion agreement. The conversion as a whole would be carried out according to a ratio of 4.5: 1, that is to say through the attribution to the banks of newly issued ordinary shares for a value of one euro for every 4.5 euros of converted credits.

The commitments of FSI and Polaris are conditioned, inter alia, upon the completion of the sale of the investments of the oil & gas sector group to the Indian group headed by Megha Engineering & Infrastructures Limited and the achievement of the restructuring agreement to be submitted to approval pursuant to article 182-bis Bankruptcy Law.

On these issues, the extraordinary assembly of Trevifin will be called to deliberate probably in May, following the ordinary assembly that will vote the budget and which was initially called for the end of April, but then postponed to wait for the definition of the restructuring agreement with the lending banks (see the press release here).

At Piazza Affari, the Trevifin stock on Thursday 19 April closed at 0.3005 euros, a decrease of 0.83% for a capitalization of 49.5 million euros, while the ExtraMot Pro-listed 50 million euros bond maturing in July 2019 and paying a 6% fixed rate coupon priced around 72 cents. The bondholders’ meeting was set for May 2 in first call and May 6 for the second call (see the press release here).

Last September Trevifin had rejected the offer of Bain Capital Credit (see here a previous post by BeBeez), which would have granted a super senior loan to the Trevi group companies operating in the foundations sector (Trevi spa and Soilmec spa) for a maximum of 100 million euro, accompanied by a conversion of the group’s existing financial debt to a variable extent, depending on the actual capital strengthening needs that would have emerged, to be implemented in the context of a debt restructuring procedure based on the art. 182-bis of the Bankruptcy Law.

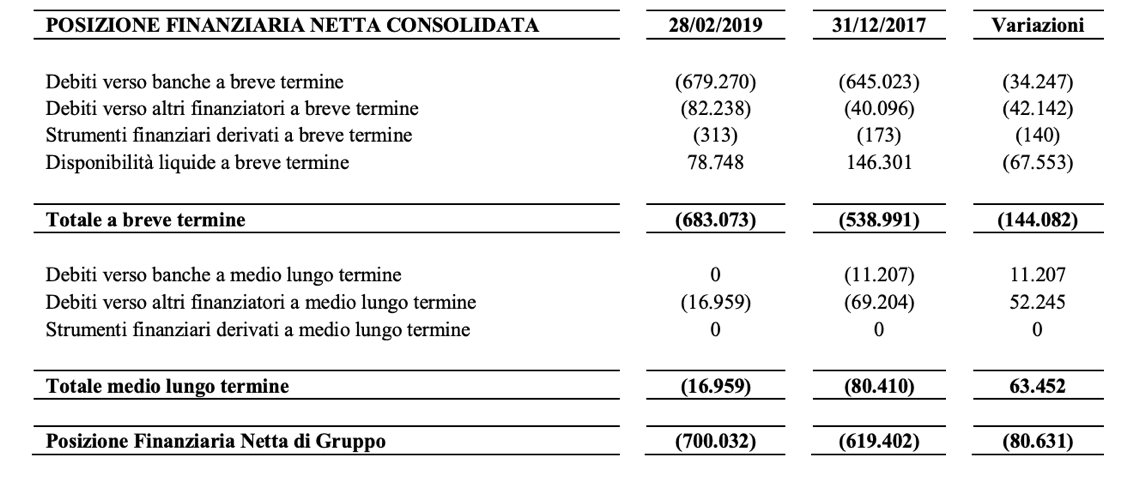

Meanwhile, at the end of February 2019 the group’s net financial position rose to 700 million euros from 619 million at the end of 2017 and from 650 million at the end of March 2018. However, these are managerial and unofficial results, because Trevi has not yet approved the financial statements as at 31 December 2017, the half-year report as at 30 June 2018, the interim report as at 30 September 2018 and the financial statements as at 31 December 2018.

The latest official figures for turnover and margins are those at the end of June 2017, when consolidated revenues had fallen to 460 million euros (from 519.3 million in the first half of 2016), mainly due to a drop of 49.3 million in the oil & gas sector, with a negative ebitda of 18.8 million, a fall of 81.2 million from a positive ebitda of 62.3 million in the first half of 2016, with the consequence of recording a net loss of 118.3 million ( from a loss of 23.6 million in the semester).

{kind=link}