Welcome to the fourth UK Property Market Stats Show of 2025, your go to weekly TV show on the UK Property Market.

This week, I am joined by the awesome Bryan Mansell, CEO of Gazeal and revered former Countrywide Regional Director in London & the SE, as we delve into the latest key property market headlines for the week ending on the 2nd February 2025.

UK Property Market Headlines for the month of January:

+ Listings in Jan ’25 up 12.9% on Jan ’24

+ Gross Sales in Jan ’25 up 19.7% on Jan ’24

+ Net Sales in Jan ’25 up 29% on Jan ’24

+ UK House Prices (on Sales Agreed) – 3.6% up on Jan ‘24

UK Property Market In-Depth Analysis for this week (Week 4)

More macro in-depth stats on the UK Property Market, ideal for those that like the hard numbers

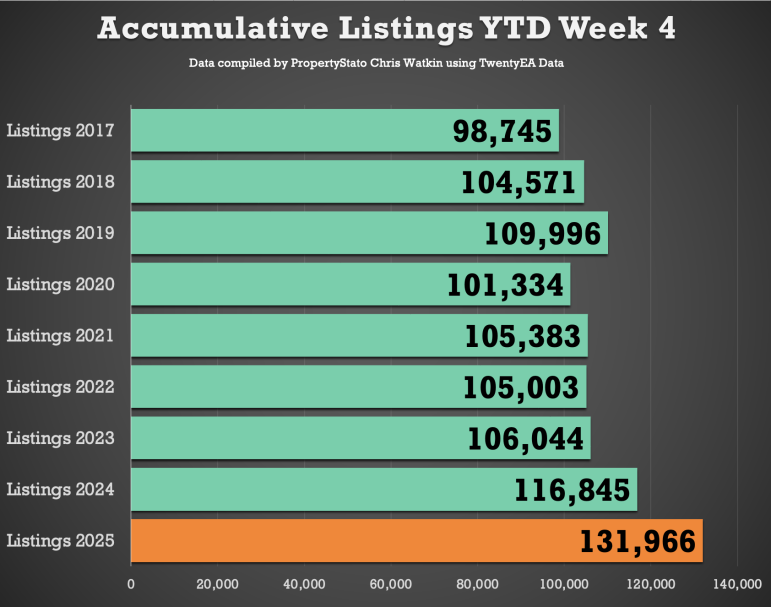

+ Listings (New Properties on the Market)

35.9k new listings this week (last week 34.9k). That’s 13% higher than Week 4 of 2024 YTD and 12% higher YTD compared to 2017/18/19.

+ Price Reductions (% of Resi Stock)

21k Price Reductions this week – meaning an approx run rate of 1 in 8 of Resi Sales stock per month is being reduced (12.1%).

For comparison, 11.9% average in 2024, though the long-term 5-year average is 10.6%.

+ Total Gross Sales (Agreed Sales)

27.5k UK homes sold STC this week, up from 25.7k last week in Week 3

That’s 29% higher YTD compared to 2024 and 37% higher than 2017/18/19 YTD levels.

+ Sale-Through Rate (Monthly in Arrears)

January’s Run rate of 15% of Resi stock sold stc. For comparison, 13.9% of residential sales stock sold in January 2025. 2024 monthly average: 15.3%. Long-term 8-year average: 17.9%.

+ Sale Fall-Throughs

6,186 Sale fall-thrus last week from Resi Sale Sales Pipeline of 440,431 homes sale agreed (sold stc).

Another method is that week’s sale fall thrus as a % of gross sales that week. This week, that is 22.5% (last week 23.3%). Slightly below the 7-year average of 24.2%, but well below the 40%+ levels post-Truss Budget (Autumn 2022).

For January ’25 as a whole, 6.03% of sales in the UK agents pipelines fell thru in Jan 25. For comparison, 2024 average: 5.36%.

+ Net Sales (Gross sales for the week less Sale Fall Thrus for the week)

21.3k net sales this week, compared to a typical week 3 average of 19.41k. Last week

Week 3 2025) – 19.7k.

2025 YTD is 29% higher than compared to 2024 YTD and 32% higher than YTD 2017/18/19.

+ Exchange to Withdrawal Ratio

53.9% of homes State agents books in January 2025, exchanged and completed. The other 46.1% left estate agents books, unsold and therefore the agent not getting paid. Overvaluing is still a huge issue in the industry.

+ Residential Sales Stock on the Market

660k properties on the market at the end of January 2025 (up, as expected, from 605k in December).

Historical comparison for end of January :

2024: 612k

2023: 525k

2022: 373k

2021: 538k

2020: 591k

2019: 614k

2018: 540k

2017: 525k.

+ Residential Sales Sold STC Pipeline

440k sales agreed but not yet completed at the end of January 2025.

Historical comparison for January :

2024: 354k

2023: 347k

2022: 447k

2021: 459k

2020: 308k

2019: 290k

2018: 282k

2017: 270k.

+ UK House Prices (£/sq.ft)

As always, the £/sq.ft metric predicts Land Registry figures 5 months in advance with 92% accuracy (the orange line of the graph).

January’s final figure: £342/sq.ft.

December ’24 : £339/sq.ft

August ’24: £334/sq.ft

January ’24: £330/sq.ft

This means UK house prices have risen 3.64% in the last 12 months. Graph 31

Local Focus – Penzance

Read the orginal article: https://propertyindustryeye.com/what-is-currently-happening-in-the-uk-property-market-40/

{kind=link}