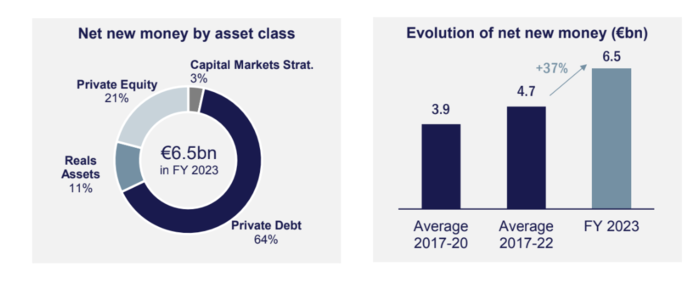

French alternative asset manager Tikehau Capital exceeds its target by reaching €42.8bn of Asset Management AuM at 31 December 2023, a 13% growth year-over-year and a 26% CAGR since 2016. Record level of net new money at €6.5bn for 2023, an amount 37% above the 2017-2022 average, reflecting the strength of the Group’s asset management platform and the relevance of its investment strategies in the current context. Cumulative net new money reaches a total of €19bn over the last 3 years and €35bn since IPO.

Tikehau Capital is reaping the benefits of its expansion strategy with:

– Complementary asset classes, serving a variety of evolving client needs and efficiently navigating the current cycle;

– An increasingly global LP base, driven by many successes recorded in 2023 across Asia, Europe, Middle East and North America, with international investors representing 54% of net inflows

– A pioneer position in the democratization of alternatives, driven by attractive and well-suited offerings across asset classes, with private investors accounting for 29% of net inflows in 2023.

Building on its multi-local platform and its solid deal sourcing capabilities, Tikehau Capital’s closed-end funds deployed €5.9bn in 2023, with an acceleration in the second half of the year. Capital deployment reached €1.7bn in Q4 2023, a stable level compared to Q3 2023.

- Private Debt accounted for 66% of total deployment, driven by the firm’s European and US CLO platform, as well as its flagship Direct Lending and Secondaries strategies. In a context of liquidity drying up, Tikehau Capital’s Direct Lending strategies have benefited from an active deal flow, attributed to the firm’s pioneer positioning, and established track record coupled with the scarcity experienced in other sources of mid-market financing. Capital deployment remained highly selective and was carried out without compromising documentation to preserve

the credit quality of portfolios. Additionally, the firm continued to structure financing solutions to facilitate bolt-on acquisitions for existing portfolio companies. In Private Debt Secondaries, the firm is well positioned to seize attractive investment opportunities, capitalizing on its early mover positioning in a context marked by active portfolio management and LPs seeking liquidity. - Private Equity accounted for 22% of total deployment, driven by thematic investments across long-term growth trends such as decarbonization, regenerative agriculture, cybersecurity and aerospace.

- The firm’s special opportunities strategy recorded a solid deployment momentum over the year, navigating a diverse range of situations and transactions, including acquisition and growth capex financing and refinancing. Beside the high level of activity, the strategy remained particularly selective with portfolio construction focusing on defensive sectors benefiting from secular trends (business services, data centers, aerospace and prime real estate). Most transactions in the portfolio also present a high degree of downside protection, illustrated by the nature of instruments and the transaction structures.

- Capital deployment across the firm’s Real Assets strategies accounted for 13% of total deployment and was spread across the firm’s European sale and leaseback practice, its European Value-Add strategy as well as granular investments for Sofidy and IREIT, the firm’s Singapore-listed REIT. Tikehau Capital has adopted a cautious and focused approach in capital deployment in Real Assets, while capitalizing on attractive investment opportunities arising from a dislocated market. Fund deployment by asset class Fund deployment evolution (€bn)

At 31 December 2023, Tikehau Capital had €6.9bn of dry powder (+13% compared to 31 December 2022), allowing the funds managed by the firm to capture attractive investment opportunities. Dry powder was mainly located within the firm’s Private Debt strategies, amounting to €2.7bn and representing 39% of the total.

Realizations within Tikehau Capital’s closed-end funds amounted to €1.9bn in 2023 (of which €0.4bn in the fourth quarter), a 5% growth year-over-year, driven by a higher level of realizations in the second half of the year. Realizations were driven by Private Debt (51% of total exits) followed by Real Assets (26%) and Private Equity (24%).

{kind=link}