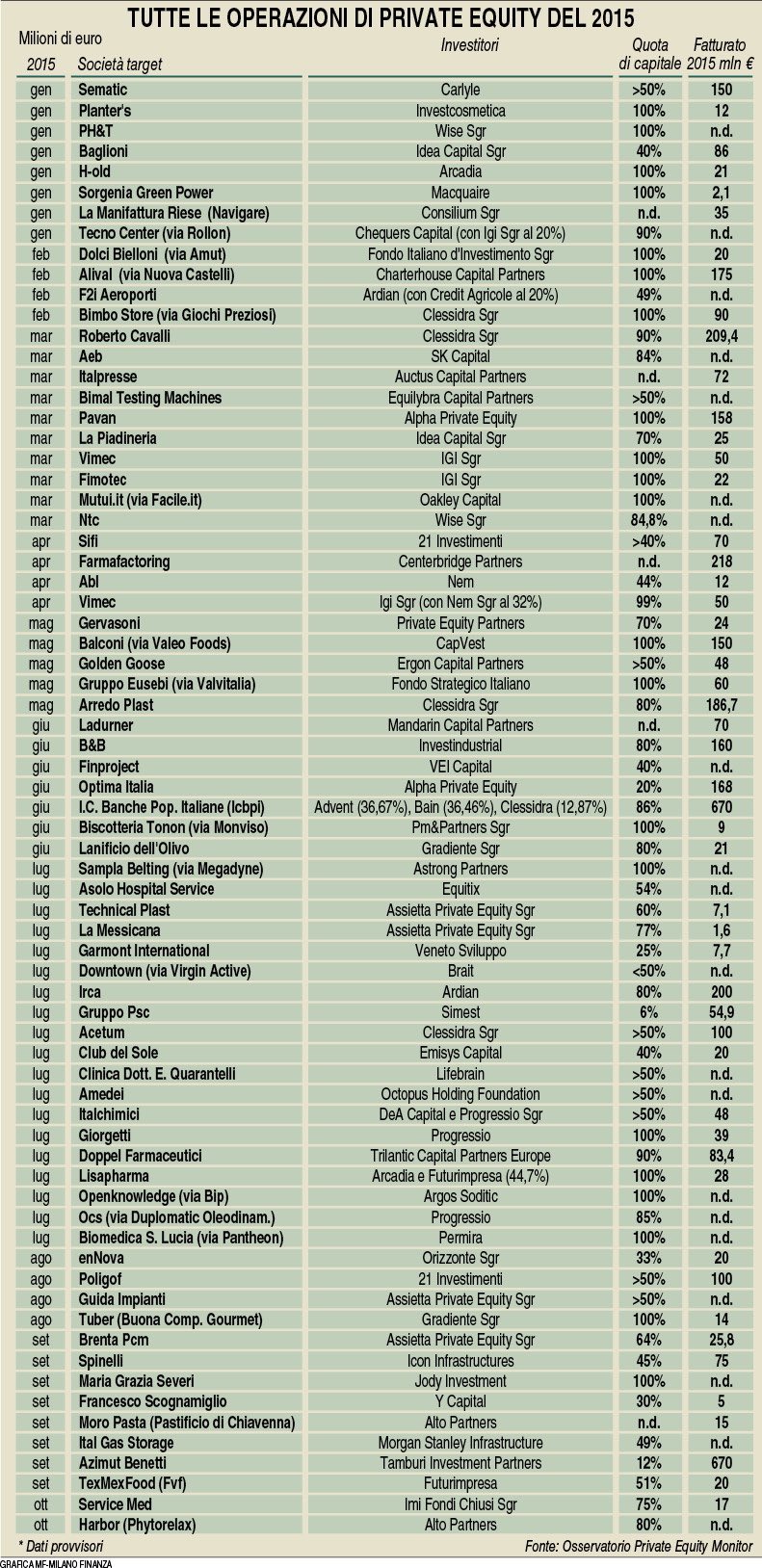

Since January 1st 2015 till mid-November private equity funds have been announcing 80 new investments in Italy versus 68 deals in the same period in 2014.

The figure is by Osservatorio Private Equity Monitor (Pem) of the Cattaneo University in Castellanza (sponsored by Argos Soditic Italia, EY, Fondo Italiano d’Investimento sgr and King&Wood Mallesons SJ Berwin) and has been published by MF Milano Finanza last Saturday January 2nd.

The 2015 figure will be even higher if you consider that since mid-November till last Christmas many other deals have been announced by private equity funds. Here follow some examples.

Italy’s leader in producing and distributing management software for businesses and professionals, Teamsystem, was acquired by Hellman&Friedman on a 1.2 billion euros valuation basis while the seller Hg Capital reinvested for a minority stake.

The global leader in the production of automatic snack and beverage vending machinese, N&W Global Vending, was bought by Lone Star. Sellers were Equistone and Investcorp for a 690 million euros valutations.

Cinven acquired Ergo Italia, a subsidiary of the German insurance group Ergo (part of Munich Re Group) which operated both life and non-life insurance products through Ergo Previdenza and Ergo Assicurazioni.

Last December Apax Partners sold for one billion euros Italy’s leading pan-European business-to-business distributor of aftermarket spare auto parts, Rhiag, to Nasdaq-listed LKQ Corporation, while Carlyle won the auction for Comdata, the leading Italian company for outsourcing of contact center, help desk and back office valued 300-350 million euros.

Among last hour’s deals you may count the acquisition of a majority stake in Banca Lecchese by Oaktree Capital Management, which bought it from Nuova Banca Etruria; a formal bid for Italy’s distressed paper manufacturer Cartiere Paolo Pigna from German holding company Bavaria Industries Group; the go-ahead by the Verona Court to Oxy Capital and Attestor Capital‘s plan to save Ferroli, a leading heating systems maker; the acquisition of iconic luxury shoes maker Sergio Rossi by Investindustrial.

Coming back to the whole 2015 year, the biggest deal was the acquisition of a 85.29% stake in Istituto Centrale delle Banche Popolari (Icbpi) for an enterprise value of 2.15 billion euros by a consortium made by Advent International, Bain Capital and Clessidra funds. Among other deals it is fair to remind the acquisition of a 90% stake in the fashion maison Cavalli by Clessidra valued 380-390 million euros; the sale of Banca Farmafactoring to Centerbridge from Apax Partners; the shareholders reorganisation of Tirrenia-Moby, as shipowner Vincenzo Onorato was supported by Och Ziff funds in buying back a 32% stake in Moby from Clessidra and in buying the whole control in Cin-Tirrenia from Clessidra itself and the minority shareholders; the sale of a 50% stake of Equita sim, one of the leading brokers active in the equity and capital markets in Italy, from JC Flowers fund to former top banker Alessandro Profumo and Equita’s managers.

Great interest from investors had two ipos of two private equity-backed companies, despite their limited market capitalization. Banca Sistema was listed last Summer and Rbs Special Opportunities fund sold all its stake in the bank’s capital; while Wise sgr sold half of its stake in the leading Italian temporary employment agency OpenjobMetis, when it was listed last December.

Anna Gervasoni, managing director of the Italian Private Equity and Venture Capital Association (Aifi) and chairman of Pem’s scientific committee at the Cattaneo University told MF Milano Finanza that “year 2015 saw a surge in private equity investments and half of them have been realized by international firms, which is quite a good sign for our market. The other half of the deal has been realized by Italian firms who target mid-size enterprises above all”.

Year 2016 will be quite active too for private equity firms in Italy. Many deals are coming where private equity firms are starring both as potential acquirors and sellers. See for example Technogym and Valvitalia‘s announced ipos and the expected ipo for Kedrion; a strategic merger planned for the European leader in payments infrastructures and technological services for banks, Sia; the announced ipo or sale of Avio Space; the coming sale of Italy’s railway stations manager Grandi Stazioni, paper manufacturer Fedrigoni, tlc services provider Sirti, catalysts and polymer materials-maker Polynt, leading Italian healthcare group in the areas of socio-medical assistance Kos, betting company Sisal, IT listed company Engineering, beer brand Peroni and minority stakes in the fashion maison maison Trussardi and the well known Naples men’s tailor Isaia.

Finally many dossier are open in the financial sector. As for the consumer credit sector, on the market are Creditis (Banca Carige), BBVA Finanzia (BBVA) and Accedo (Intesa Sanpaolo), while auctions are opening for the asset manager Arca sgr and investment bank GE Capital Interbanca. Finally Bank of Italy announced last December 30th that a sale process is starting for the four new “good banks” which were spun off from four mid-size distressed banks last November (Npls and subordinated debt had been moved to a unique bad bank instead). on sale are Nuova Banca delle Marche, Nuova Banca dell’Etruria e del Lazio, Nuova Cassa di Risparmio di Chieti and Nuova Cassa di Risparmio di Ferrara.

{kind=link}