The index of Argos Wityu and Epsilon Research monitors the valuation multiples of the Euro area SMEs that sold a majority stake in the previous six months.

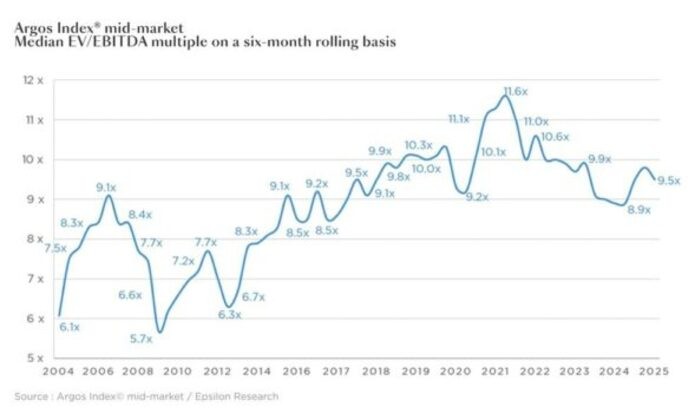

Argos Index mid-market, a metric that pan-European private equity Argos Wityu and software, data and analysis provider for M&A, Private Equity and valuation markets Epsilon Research created in 2006, says that 1Q25 median EV/ebitda over 6 moving months multiple of unlisted Euro area SMEs that sponsors targeted dropped to 9.5X ebitda, down 3% from 9.8X in 4Q24 (press release, 4Q24 and Q25 Report). A recent KPMG report said that in 2024, the M&A and private equity market inverted the previous two years negative trend (see here a previous post byBeBeez). A recent KPMG report said that in 2024, the M&A and private equity market inverted the previous two years negative trend (see here a previous post byBeBeez).

Argos Index monitors the valuation trends for the unlisted SMEs of the Euro area that sold a majority stake in the previous six months.

However, in 1Q25, financial sponsors paid 0.8X Ebitda more than strategic investors, in line with 2021 median value.

In 1Q25, trade buyers paid 9.2X ebitda multiples (9.3X in 4Q24) for acquisitions while financial sponsors purchased assets for 10X (10.3X in 4Q24). In 2024 the volume of private equity investments plummeted for the first time in two decades as funds were under pressure to sell assets and return liquidity to their Limited Partners (see here the BeBeez Insight Views about the data of Bain & Co, McKinsey, PitchBook, and Preqin, available for the subscribers to BeBeez News Premium and BeBeez Private Data). The stock markets’ volatility that Donald Trump’s threat for tariffs triggered made negotiations more difficult. However, to the ongoing improvement of big caps’ financial health and their interest in transformational acquisitions limited the impact of announced international trade restrictions. Stefania Peveraro, BeBeez Editor in Chief, highlighted that financial sponsors are investing in continuation funds for the current volatile context (see here a previous post by BeBeez).

In 1Q25, 32% of transactions closed at below 7X or above 15X, down 33% from 4Q24, the trough since Covid related turmoil. Deals closed at above 15X are 9% of analysed transactions (13%in 4Q24). Acquisitions at below 7X make 23% of total volume (+20% since 4Q24).

Louis Godron, the chairman of Argos Wityu, said: “Growing uncertainty regarding the US administration’s economic and trade policies caused a stall in the mid-market recovery in the Euro area, a reduction in m&a activity and increased market volatility. Despite lower borrowing costs, expectations of further rate cuts by the ECB, easier access to finance and declining attractiveness approaching the 2% target, the decline in euro-area SME valuations in 1Q25 reflects widespread concern, and optimistic forecasts are now a thing of the past”.

{kind=link}