In 2024, the buyout firms invested in the region of 1.5 billion with a median entry value of 11.9X ebitda. It is the second highest figure ever recorded.

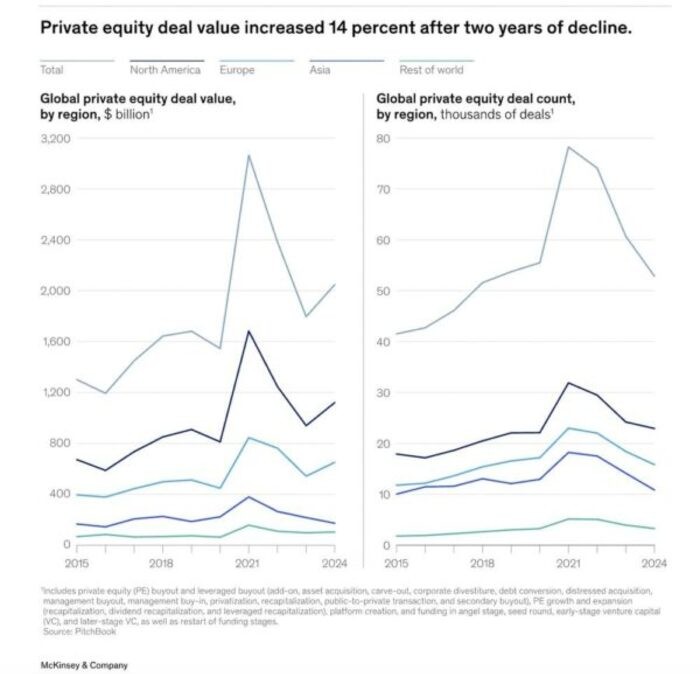

McKinsey Global Private Markets Report 2025 (Private equity emerging from the fog) said that 2024 has been the third most active year in the history of the industry as private equity and venture capital global investments increased by 14% yoy for a total of 2 trillion US Dollars.

The report aggregated and rielaborated SPI by Stepstone, Preqin and PitchBook data which highlight that a few factors helped the sector to rebound and improve expectations. Buyout’s entry multiples reached again the 2021-2022 level. The global median EV/ebitda buyout multiple amounted to 11.9X, the second highest ever recorded after the 12X peak of 2022. Buyout funds valued their targets at significantly higher prices than in 2023.

The report says that key drivers for the increase of such multiples are:

- Better financing conditions: the cost of debt for acquisitions fallen from its 2023 peaks, but it is still higher than the 10-year average.

- Better quality of the assets up for sale: Many funds sold companies with stronger financials and high growth prospects, increasing market valuations.

- Bidders competing again: As economic uncertainty decreased, funds started again to contending each other for the best opportunities, pushing up prices.

The aggregate value of buyout transactions is 1.5 trillion from just over 1.2 trillion in 2023. Transactions above 500 million have gone up 37% in value and 3% in number, indicating a greater appetite for funds to invest in larger companies. This was particularly evident in North America and Europe, while the Asian market contracted.

Public-to-private (P2P) or delisting transactions of private equity funds accounted for 11% of the total value of global deals compared to 9% in 2023. Europe saw a 65% yoy increase in the value of these operations, with US sponsors (almost 75% of P2Ps by value over the past five years, up from just 50% in the previous decade) increasingly active. In 2024, global market participants carried on the second highest number of P2P transactions.

In 1H24, global dry powder decreased by 11% to 2.1 trillion as funds allocated again resources for new deals and reduced the idle time of capital raised. However, dry powder is still at high levels, still representing 1.89 years of investment reserves compared to the annual utilisation rate. This means that funds have almost two years of ready to invest capital, suggesting that the M&A pace could remain strong in 2025.

However, the McKinsey report says that the private equity industry is still facing challenges:

- The average holding time of portfolio companies increased to 6.7 years, compared to an average of 5.7 years over the past two decades. This suggests a slowdown in the exit process, with many funds remaining stuck on investments made in previous years at high valuations.

- The backlog of portfolio companies awaiting exit is the highest since 2005.

- Persistent geopolitical uncertainty: expected increases in trade tariffs and evolving international tensions could affect the sector in the coming years.

In conclusion, 2024 marked a major upswing for private equity, with a return to investment, an increase in valuation multiples and greater confidence in the industry. However, the market will face challenges related to exits, liquidity and the ability to generate operating value to support future growth.

{kind=link}