Meanwhile, the Piazza Affari-listed paytech group closes 9 months 2023 with rising revenues and profitability. The stock at the beginning of today’s session marks +6.4 percent

While rumors of international private equity funds’ interest in Nexi continue to chase each other (see here a previous article by BeBeez International), the Milan-listed paytech group this morning released its results for the nine months 2023, which were good and in line with expectations, and announced the sale of the eID business that provides digital identity solutions in the Nordic countries to banks, corporations and the public sector: Buying in is the French public IN Groupe, a leading global provider of secure digital identities and services (see the press release here and the analyst presentation here).

The sale of the Nordic eID business will take place for a maximum consideration of €127.5 million, including an upfront component of €90 million and up to a maximum of €37.5 million in the form of earn-outs, contingent on the achievement of certain financial targets. This business, which has already been reclassified as an asset held for sale since the beginning of the year, is expected to generate about 11 million euros in run-rate ebitda in 2023. The transaction is expected to close by Summer 2024, subject to several conditions precedent, including regulatory approval in Denmark.

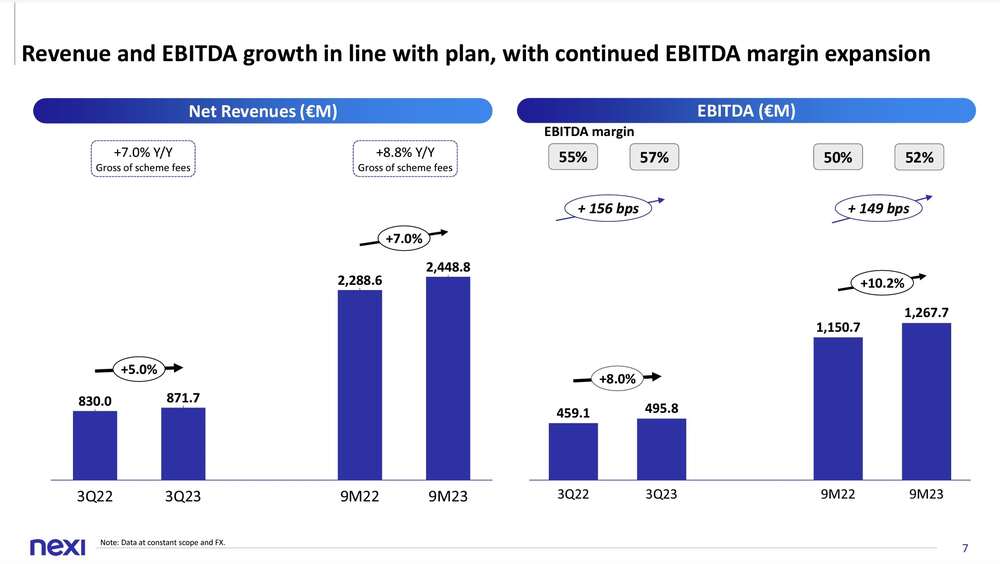

As for the nine-month results, revenues stood at 2, 45 billion euros (+7% from nine months 2022), with an ebitda of just under 1.27 billion (+10.2%) and an ebitda margin of 52% (+ 149 basis points), against a net financial debt down to 5.35 billion and a NFP to ebitda ratio down to 3.1x, which becomes 2.8x pro-forma if run-rate synergies are included. Finally, year-end guidance is confirmed, meaning revenue growth of more than 7 percent, ebitda growth of more than 10 percent, excess cash generation of at least 600 million, and net financial leverage of 2.9x ebitda (2.6x pro-forma, all with normalized earnings per share up more than 10 percent.

Recall that 2022, on the other hand, had closed with 3.26 billion in revenues (+7.1% from 2021), ebitda of 1.613 billion (+14.2%) and net financial debt of 5.396 billion, with leverage therefore of 3.3 times or 2.9 times pro-forma (see the press release here).

As for possible offers from new investors coming in, recall that today Nexi’s shareholding structure is firmly in the hands of private equity funds. In fact, the first shareholder is the Hellmann & Friedman fund with 19.94%, followed by the Italian National Promotional Institution CDP Equity with 13.57%; then with 9.42% is Mercury UK, a company that groups the holdings of the private equity funds Advent International, Bain Capital and Clessidra, who used to be the group’s reference shareholders before Nexi was listed on the Milan Stock Exchange (see here a previous article by BeBeez); and finally, with 2a .12% stake, is GIC, SIngapore’s sovereign fund.

As a reminder, following the July 1, 2021 merger of Denmark’s Nets into Nexi (see the press release here), Nets’ shareholder funds (Hellmann & Friedman, GIC, Bain Capital, and Advent International) had reinvested in Nexi and thus became shareholders of the MIlan-listed group. The paytech’s shareholder base then evolved further at the time of the merger with Italy’s SIA, a group focused on infrastructures for electronic payments (see here a previous article by BeBeez). SIA’s main shareholder was in fact CDP Equity, with 82.8 percent, joined by Poste Italiane with 17.2 percent. Following the merger, effective as of early 2022 (see the press release here), both CDP Equity and Poste Italiane found themselves partners in Nexi.

For some time, depressed market prices, in the face of a business that is instead going strong, have attracted the interest of international private equity funds. It had already happened last year, when there were talks of negotiations with Silverlake (see here a previous article by BeBeez), while in mid-October there was talk of a potential offer coming from CVC Capital Partners (see here a previous article by BeBeez International). Since then the Silverlake hypothesis has also been back in vogue, while the names of Brookfield, CPP Investments (Canada Pension Plan Investment Board) and Francisco Partners are circulating these days (see MF Milano Finanza).

Yesterday Nexi’s stock closed the Stock Exchange session on Euronext Milan at 5.998 euros per share, after hitting an all-time low last October 27 at 5.372 euros. A figure that compares with the all-time high marked at 19.40 euros per share in July 2021. The descent of the stock price, therefore, has been really huge, driven by an environment that as known in the last two years has been particularly heavy for the entire tech sector, after the valuation peaks touched in 2021. This morning Nexi’s stock opened in the air, currently trading above 6.38 euros with an appreciation of 6.4 per cent.

{kind=link}