It happened in mid-August 2022 and now again. The paytech Nexi, listed on Piazza Affari, is attracting the sights of private equity funds, due to depressed market prices, in the face of a business that is instead going strong (see a previous article by BeBeez). Yesterday evening, the hypothesis was re-launched by Bloomberg, which spoke of a potential offer coming from CVC Capital Partners. The latter is a private equity giant that, in turn, has in recent weeks been the subject of persistent rumours about a listing project on Euronext Amsterdam, which could be unveiled in the coming days (see a previous article by BeBeez).

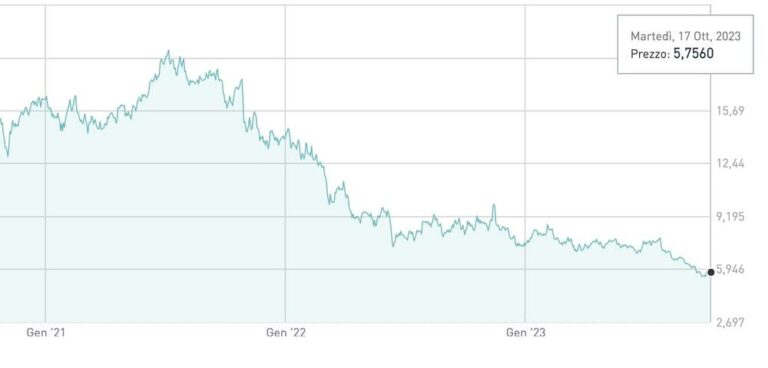

What attracted the interest of CVC, which could act in tandem with a co-investor, perhaps with Silverlake (see a previous article by BeBeez), which was rumoured to have been in talks with Nexi’s shareholders at the beginning of 2022, were the group’s quotations, which yesterday closed the stock exchange session with +0.1% at EUR 5.756 per share, slightly above the all-time low reached on 9 October at EUR 5.482, for a capitalisation of just over EUR 7.55 billion. A figure that compares with the all-time high set at EUR 19.40 per share in July 2021. The fall in share prices, therefore, was truly enormous, driven by an environment that, as is well known, in the last two years has been particularly heavy for the entire tech sector, after the valuation peaks touched in 2021.

At the same time, as mentioned, Nexi grew significantly on the business front and also conducted an aggressive m&a campaign. The latest acquisition was announced last February, when Nexi signed an agreement to acquire 80% of its merchant acquiring business from the Spanish Banco Sabadell on the basis of an enterprise value for 100% of €350 million (see here a previous article by BeBeez). In June 2022, on the other hand, the group had reached an agreement with BPER on a strategic partnership in the field of payment cards (see here a previous article by BeBeez).

In fact, the two groups signed a contract to transfer to Nexi Payments the merchant acquiring (the activity that allows customers’ cards to be debited and merchants’ accounts to be credited) and POS management of BPER and Banco di Sardegna. At the same time, Nexi acquired 100% of Numera Sistemi e Informatica from Banco di Sardegna, after carve-out from Numera itself of the activities not related to POS management and assistance.Still on the subject of merchant acquiring, in August 2021 Nexi had signed a strategic partnership with Alpha Services and Holdings, the parent company of the Greek bank Alpha Bank, thanks to which the Greek bank promotes and distributes the solutions developed by Nexi to its customers (see here a previous article by BeBeez). Even earlier, in December 2019, Nexi had bought the merchant acquiring business of Intesa Sanpaolo, which had sold the related business unit for EUR 1 billion against the purchase by the same bank of a 9.9 per cent stake (see here a previous article by BeBeez). Subsequently, the bank had diluted itself to 5.12%, following the merger between Nexi and Nets, and finally, last November, it sold its share on the market, exiting the capital (see here a previous article by BeBeez).

To date, Nexi’s shareholding structure is still firmly in the hands of private equity funds. The first shareholder is in fact the Hellmann & Friedman fund with 19.94%, followed by CDP Equity with 13.57%; then there is Mercury UK with 9.42%, the holding company that groups together the holdings of the private equity funds Advent International, Bain Capital and Clessidra, which, prior to the paytech’s listing on PIazza Affari, were its reference shareholders (see here a previous article by BeBeez); and finally there is GIC, the sovereign fund of Singapore, with 2.12%.

As a reminder, following the merger of the Danish Nets into Nexi on 1 July 2021 (see the press release here), Nets’ fund shareholders (Hellmann & Friedman, GIC, Bain Capital and Advent International) reinvested and thus became shareholders in Nexi. The paytech’s shareholder structure then evolved further to coincide with the merger with SIA (see here a previous article by BeBeez). SIA’s main shareholder was in fact CDP Equity, with 82.8%, alongside Poste Italiane with 17.2%. Following the merger, effective from the beginning of 2022 (see the press release here), both became shareholders of Nexi.

In terms of financial results, the group closed the first half of 2023 with EUR 1.577 billion in revenues (+8.1% from the first half of 2022), an ebitda of EUR 771.8 million (+11.6%) and a net financial debt of EUR 5.422 billion, which implies a leverage of 3.2 times, which on a pro-forma level (including run-rate synergies) is instead around 2.8 times. Numbers that led the group to indicate year-end guidance of 7% growth in revenues from 2022 and 10% growth in ebitda, against 3 times or 2.7 times pro-forma leverage (see the press release here). In contrast, 2022 had ended with 3.26 billion in revenues (+7.1% from 2021), an ebitda of 1.613 billion (+14.2%) and a net financial debt of 5.396 billion, with leverage therefore of 3.3 times or 2.9 times pro-forma (see the press release here).

But if these are the results, it is really unlikely that Nexi’s shareholder funds would want to sell off the group at current prices. Perhaps it is reasonable to imagine that what is now a well-established practice in the world of large buyout operators could be followed, which when they find themselves with assets in their portfolio that they still consider very interesting but which are now dated for a fund that is perhaps nearing the end of its life, they decide to launch a so-called continuation fund and hand over the asset in question, with the support of old and new investors who are specialists in the secondary market.

{kind=link}