How many non-performing loans the new Italian government-sponsored Atlante fund will be able to remove from Italian banks’ books? MF Milano Finanza tried to figure out a number on the basis of the available information and the result is a maximum of 27 billion euros that is rather lower than the 50 billion euros that italy’s Ministry for Economy and Finance Pier Carlo Padoan talked about in an interview released to Class Cnbc tv channel a couple of days ago, And obviously is much more lower than the 80 billion euros of net Npls of the whole Italian banking system.

How many non-performing loans the new Italian government-sponsored Atlante fund will be able to remove from Italian banks’ books? MF Milano Finanza tried to figure out a number on the basis of the available information and the result is a maximum of 27 billion euros that is rather lower than the 50 billion euros that italy’s Ministry for Economy and Finance Pier Carlo Padoan talked about in an interview released to Class Cnbc tv channel a couple of days ago, And obviously is much more lower than the 80 billion euros of net Npls of the whole Italian banking system.

These concepts are stressed in some reports from US investment banks and rating gencies in the last few days which are particularly severe with the Atalnte project. See here reports from Bernstein, Standard&Poor’s, Morgan Stanley and Fitch.

However this severe position against Atlante fund seems to be an answer to a menace as US credit funds had represented the majority of the acquirors of Italian Npls in the last few years at prices that are about 25-30% of gross value for secured Npls or about 2-5% of gross value for unsecured Npls. On the contrary it is understood that Atlante fund will value Npls at prices close to the net value on the Npls on the banks’ books in a way not to cause new losses to banks (see here a previous post by BeBeez).

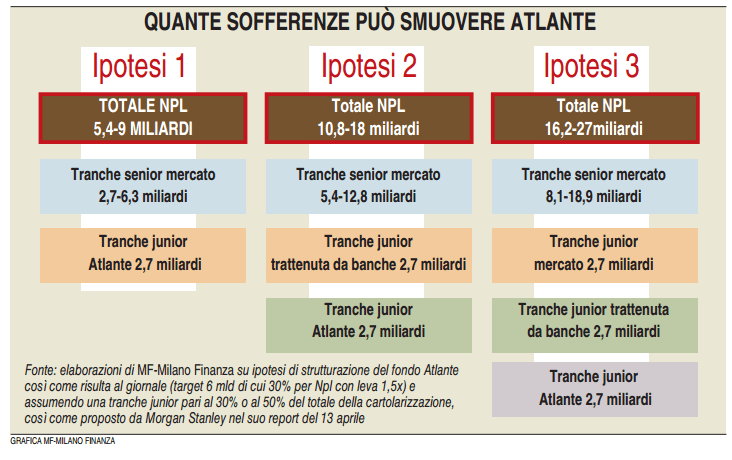

The 27 billion euros figure comes out from the following considerations. First of all the fund target is said to be 6 billion euros of which about 70% will be deployed in subscribing Italian banks’ capital increases as a back stop facility. As for the other 30% or 1.8 billion euros, this might be leveraged to 1.5x so to become 2.7 billions and will be deployed in subscribing equity tranches of Npls securitizations at a price value which is about the same of the net book value.

Assuming the equity tranches 30-50% of the total Npls, it is possibile to imagine that the fund will buy it all or just a 50% with the originator banks retaining the other 50%. It is possible also to imagine that other investors decide to join the deal and buy part of the equity tranche (in MF Milano Finanza example they buy one third, while the othre two thirds are bought by Atlante and the originator banks). As for the senior tranches (70% or 50% of the total securitization), they would be offered to the market with a guarantee from the Italian government (Gacs). In the best scenario then the deal would involve removing about 27 billion euros Npls from Italian banks’ books. While the wrost sees just 5,4 billion euros of Npls sold.

An idea fromattracting investors into the equity tranches and so enhance to size of the whole deal might be to structure turanround deals whenever is possibile relating to corporate Npls. If a securitization seal is structured on corporates’ debt while a private equity fund inject new fresh finance for relauching the coporate’s business, a recovery in the Npls value is quite more probable. Among Npls actually are counted all corporates that are passing through a backrupcty procedure.

{kind=link}